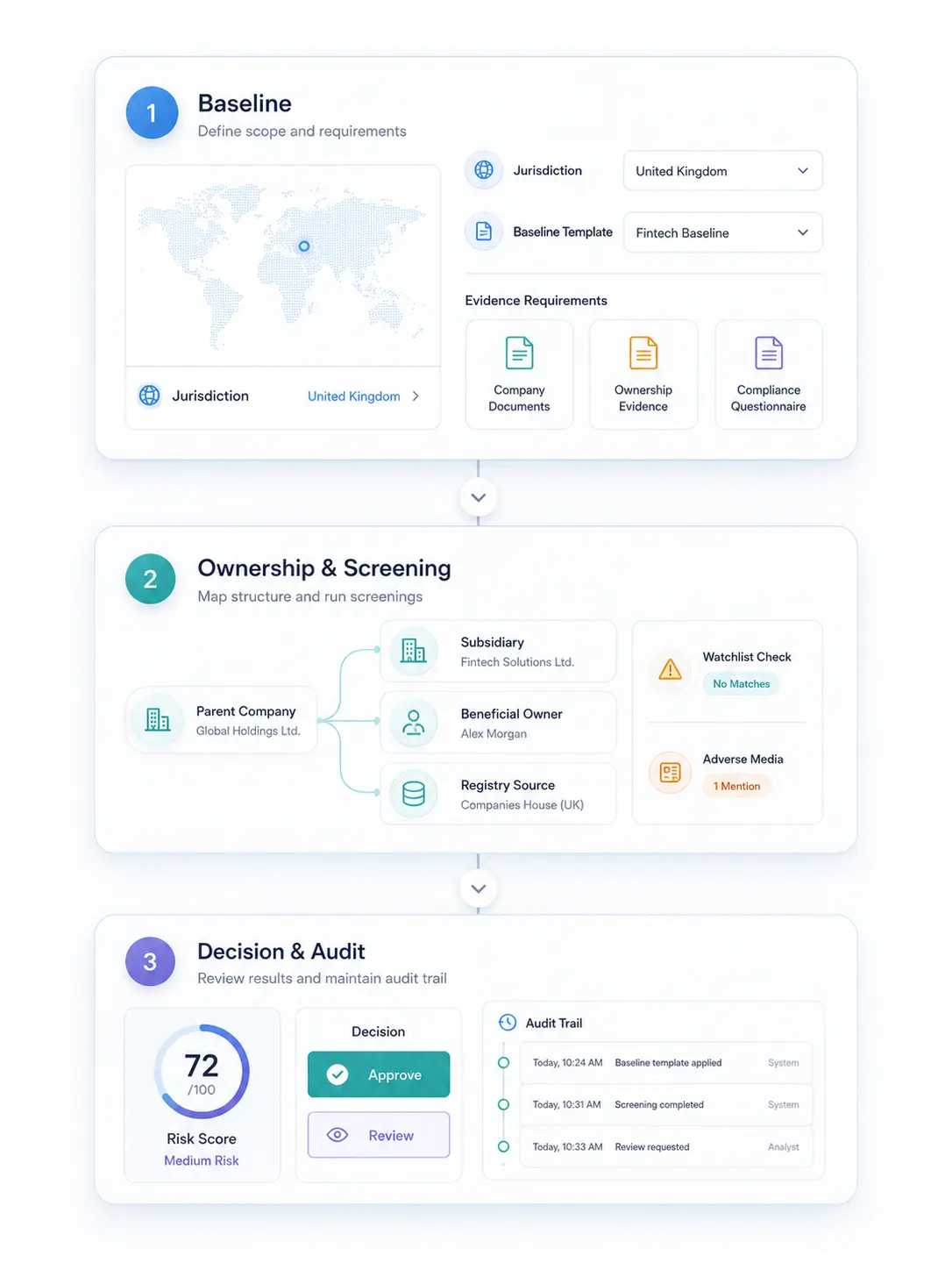

Run risk-based KYB remotely with structured evidence and explainable decisions. Verify ownership confidently, route edge cases, and keep risk updated over time.

Pick a jurisdiction template, required evidence, and review thresholds for business onboarding.

Map UBO structures, validate registry data, and flag watchlist or adverse media signals.

Auto-approve low risk, route edge cases, and keep a complete evidence trail for audits.

A risk-based baseline for business onboarding, remote verification, and audit-ready evidence.

* Use this as a starting point. Requirements vary by jurisdiction and risk profile.

Common signals in remote onboarding and ownership verification that require extra scrutiny

Multi-layer entities, cross-border control, missing or changing UBOs.

Name, status, directors, or addresses don’t reconcile across sources.

Low-assurance flows, unusual patterns, or gaps in verification evidence.

Potential sanctions or PEP relevance that needs confirmation and notes.

Jurisdiction exposure that changes the required evidence or thresholds.

Recent or high-severity allegations that require documented rationale.

Faster onboarding, lower manual effort, and audit-ready evidence with a risk-based workflow

Real questions from compliance teams evaluating Detelio. If something's missing, ask us in the demo — we'd rather over-share.

KYB verifies a business and its control structure (registration, directors, beneficial owners, risk signals). KYC verifies the individual. In fintech onboarding, you often need both because businesses have natural persons behind them and ongoing exposure changes over time.

It means your onboarding steps and evidence requirements change based on risk. Remote flows should be designed and assessed to remain safe and effective under AML/CFT expectations, with appropriate controls for the tools you use.

You typically need enough information to identify the true owners and controllers of the company, and keep it adequate, accurate, and up to date. The right “how” varies by jurisdiction, but the core principle is reliable access to beneficial ownership information.

Digital ID can support customer identification and verification in a risk-based way. Trustworthy digital IDs can reduce risk and make identification easier, cheaper, and more secure when appropriate mitigations are in place.

Escalate when signals suggest higher ML/TF risk: complex ownership chains, registry inconsistencies, watchlist proximity, high-risk jurisdictions or corridors, severe adverse media, or low-assurance remote onboarding signals. (Keep your triggers consistent with your risk-based policy.)

A clear evidence pack that shows what checks ran, what sources were used, what was found, who approved what, and why. For remote onboarding, keeping an auditable trail of how your onboarding solution was used and assessed is part of demonstrating effective controls.

Use ongoing, risk-based monitoring: recheck on meaningful changes like registry updates, ownership changes, new watchlist hits, or changes in expected activity. This keeps beneficial ownership info and risk posture current.

No. Use this page as a starting baseline, then align it to your regulator, licenses, products, and risk appetite.

Built for risk-based remote onboarding and audit-ready KYB evidence